When it comes to energy security, Central Asian governments have shown an ability to adapt to shifting global and domestic trends. Just as renewable energy has overtaken coal as the major source of electricity globally for the first time in history, Central Asian countries are struggling to balance their Paris Agreement commitments with the economic realities. From Kazakhstan’s U-turn on coal to Central Asia’s embrace of nuclear energy, the recent developments in the renewable energy sector reflect both global currents – from the U.S. president’s disdain for climate change consensus to rising energy demands of AI hyperscalers – and domestic economic and infrastructural realities.

The Nuclear Option

As renewables introduce greater inflexibility into power systems and subsidies strain fiscal accounts, Central Asian governments are seeking middle-ground solutions that reconcile fiscal and environmental priorities. From this point of view, nuclear power offers an appealing alternative – neither as intermittent as renewables nor as emission-intensive as hydrocarbons, and grounded in the region’s rich uranium endowments.

Last year Kazakhstan and Uzbekistan, the first and and the fifth largest global suppliers of uranium, respectively, overcame their historical reluctance to nuclear energy adoption. Kazakhstan held a national referendum on nuclear energy in October 2024 and Uzbekistan announced in May 2024 it would construct a smaller scale nuclear power plant (NPP) installation based on small modular reactors (SMRs).

Since then both countries have greatly expanded their nuclear ambitions. Kazakhstan announced that it will build not one but three NPPs, allowing the country to offset the inherently geopolitical aspect of long-term dependency on partner countries with one contract granted to Russia’s Rosatom and two other plants likely to be awarded to China’s CNNC. In turn, Uzbekistan’s initial plan to build a 300 MW plant based on Rosatom’s SMRs has been revised to incorporate two large 1000 MW reactors, taking the site production capacity to 2100 MW.

Securing funding for NPP expansion, however, might become a complex political and economic issue. The initial SMR stage of the NPP in Uzbekistan’s Jizzakh region was estimated at around $1 billion, fully funded by the state; the projected expansion would require massive additional investments. For comparison, Rosatom’s 2.4 GW NPP in Kazakhstan is projected to cost about $14 billion, largely funded by an interstate loan from Russia.

Cost and time overruns, typical for nuclear construction worldwide, further complicate the outlook. A recent global study showed that an average nuclear power plant faces a construction cost overrun of $1.5 billion and a time overrun of 35 months. For both Kazakhstan and Uzbekistan, nuclear power holds strategic promise, but its long construction timelines and high costs make it a viable medium- to long-term option rather than an immediate solution to the countries’ energy security and decarbonization needs.

Last year Kazakhstan and Uzbekistan, the first and and the fifth largest global suppliers of uranium, respectively, overcame their historical reluctance to nuclear energy adoption. Kazakhstan held a national referendum on nuclear energy in October 2024 and Uzbekistan announced in May 2024 it would construct a smaller scale nuclear power plant (NPP) installation based on small modular reactors (SMRs).

Since then both countries have greatly expanded their nuclear ambitions. Kazakhstan announced that it will build not one but three NPPs, allowing the country to offset the inherently geopolitical aspect of long-term dependency on partner countries with one contract granted to Russia’s Rosatom and two other plants likely to be awarded to China’s CNNC. In turn, Uzbekistan’s initial plan to build a 300 MW plant based on Rosatom’s SMRs has been revised to incorporate two large 1000 MW reactors, taking the site production capacity to 2100 MW.

Securing funding for NPP expansion, however, might become a complex political and economic issue. The initial SMR stage of the NPP in Uzbekistan’s Jizzakh region was estimated at around $1 billion, fully funded by the state; the projected expansion would require massive additional investments. For comparison, Rosatom’s 2.4 GW NPP in Kazakhstan is projected to cost about $14 billion, largely funded by an interstate loan from Russia.

Cost and time overruns, typical for nuclear construction worldwide, further complicate the outlook. A recent global study showed that an average nuclear power plant faces a construction cost overrun of $1.5 billion and a time overrun of 35 months. For both Kazakhstan and Uzbekistan, nuclear power holds strategic promise, but its long construction timelines and high costs make it a viable medium- to long-term option rather than an immediate solution to the countries’ energy security and decarbonization needs.

Fitting Renewables into the Central Asian Energy Mix

Uzbekistan has traditionally relied on its own gas reserves to supply its thermal power plants. But with plummeting gas extraction and rising electricity consumption, its gas imports exceeded exports last year by about $1 billion. The gas-burning thermal plants in Tashkent, the country’s largest population and economic center, are ill-suited for the use of alternative fuels. During the colder winter months, persistent gas shortages result in electricity blackouts and disruptions of gas supply to homes and refueling stations for cars refitted with popular compressed natural gas engines. The coal-firing plants around the capital pump hundreds of thousands of tonnes of emission into the atmosphere. Each winter Tashkent faces a harsh choice between keeping the lights on and the air clean.

Renewables are thus seen not just as a viable, but as a better alternative to hydrocarbons. By September 2025 Uzbekistan reported a record of 8 billion kWh of electricity generated by solar and wind, which combined with hydropower accounted for over 20 percent of the country’s energy generation. Earlier, Global Energy Monitor data showed that by late 2024 Uzbekistan had the largest absolute volume of renewable capacity in development in Central Asia and the Caucasus.

The bulk of this capacity is accumulated by Saudi ACWA Power’s $15 billion investment portfolio in Uzbekistan, including Central Asia’s first green hydrogen plant and its largest battery energy storage system (BESS) facility. ACWA Power managed to attract large-scale internationally syndicated financing from a variety of institutional investors, with the tacit acceptance by the government that higher levels of foreign debt, exceeding $72 billion by the first half of 2025, are essential for the country’s economic and infrastructural development.

Kazakhstan’s situation is radically different. Having the tenth largest coal reserves in the world, the country consumes domestically only a fraction of its production. With coal as a primary source of power generation, accounting for 54 percent of the country’s electricity, Kazakhstan has ample and secure supply to power itself for many decades to come, even taking into account the nation’s ambitious plans to become a regional data processing and AI hub. Coal expansion and the addition of nuclear power to the country’s energy mix may potentially close the gap between domestic production and consumption, and free up significant volumes of natural gas, currently accounting for almost 30 percent of electricity generation, for export.

The transition to renewables for Kazakhstan has therefore been a matter of political choice, not economic necessity. To deliver on its Paris Agreement and its own Carbon Neutrality Strategy commitments of achieving 15 percent share of renewable generation by 2030, the country of vast steppes is actively exploring its massive wind energy potential. The almost negligible share of wind energy in the late 2010s has since grown to 4 percent of total power generation (or almost half of hydropower share), driven by the expedited construction of large scale wind farms. These include the most recent opening of a 150 MW, 24-turbine wind farm in Aktobe region, one of the region’s largest, and the massive 1 GW project by TotalEnergies in Zhambyl region planned for launch in 2028.

This transition, however, comes at a price. To achieve 2030 goals the Kazakh government estimates it would require around $10 billion of additional investments, while the government continues to subsidize renewable generation by sustaining RES tariffs at levels 2-3 times higher than those of the country’s thermal plants. Hence, President Kassym-Jomart Tokayev’s public endorsement of U.S. President Donald Trump’s policy of “beautiful clean coal” powering American industry and data centers is not a merely diplomatic maneuver aimed to strengthen growing Kazakh-U.S. ties but a sober reflection of Kazakhstan’s own economic realities.

Renewables are thus seen not just as a viable, but as a better alternative to hydrocarbons. By September 2025 Uzbekistan reported a record of 8 billion kWh of electricity generated by solar and wind, which combined with hydropower accounted for over 20 percent of the country’s energy generation. Earlier, Global Energy Monitor data showed that by late 2024 Uzbekistan had the largest absolute volume of renewable capacity in development in Central Asia and the Caucasus.

The bulk of this capacity is accumulated by Saudi ACWA Power’s $15 billion investment portfolio in Uzbekistan, including Central Asia’s first green hydrogen plant and its largest battery energy storage system (BESS) facility. ACWA Power managed to attract large-scale internationally syndicated financing from a variety of institutional investors, with the tacit acceptance by the government that higher levels of foreign debt, exceeding $72 billion by the first half of 2025, are essential for the country’s economic and infrastructural development.

Kazakhstan’s situation is radically different. Having the tenth largest coal reserves in the world, the country consumes domestically only a fraction of its production. With coal as a primary source of power generation, accounting for 54 percent of the country’s electricity, Kazakhstan has ample and secure supply to power itself for many decades to come, even taking into account the nation’s ambitious plans to become a regional data processing and AI hub. Coal expansion and the addition of nuclear power to the country’s energy mix may potentially close the gap between domestic production and consumption, and free up significant volumes of natural gas, currently accounting for almost 30 percent of electricity generation, for export.

The transition to renewables for Kazakhstan has therefore been a matter of political choice, not economic necessity. To deliver on its Paris Agreement and its own Carbon Neutrality Strategy commitments of achieving 15 percent share of renewable generation by 2030, the country of vast steppes is actively exploring its massive wind energy potential. The almost negligible share of wind energy in the late 2010s has since grown to 4 percent of total power generation (or almost half of hydropower share), driven by the expedited construction of large scale wind farms. These include the most recent opening of a 150 MW, 24-turbine wind farm in Aktobe region, one of the region’s largest, and the massive 1 GW project by TotalEnergies in Zhambyl region planned for launch in 2028.

This transition, however, comes at a price. To achieve 2030 goals the Kazakh government estimates it would require around $10 billion of additional investments, while the government continues to subsidize renewable generation by sustaining RES tariffs at levels 2-3 times higher than those of the country’s thermal plants. Hence, President Kassym-Jomart Tokayev’s public endorsement of U.S. President Donald Trump’s policy of “beautiful clean coal” powering American industry and data centers is not a merely diplomatic maneuver aimed to strengthen growing Kazakh-U.S. ties but a sober reflection of Kazakhstan’s own economic realities.

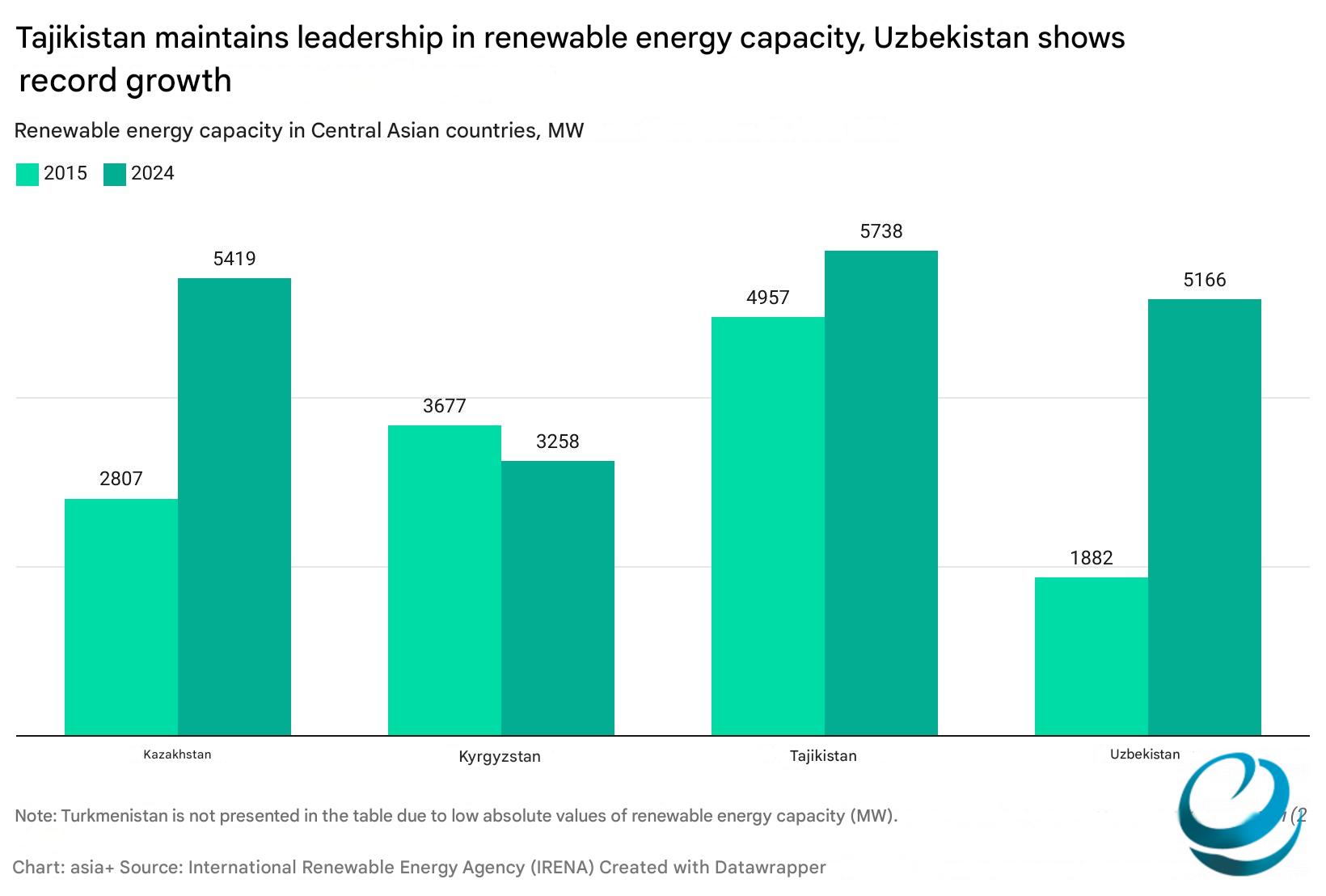

Renewable Energy Champions

Data source: www.centralasiaclimateportal.org

The region’s renewable energy champions, Kyrgyzstan and Tajikistan – where hydropower accounts for the lion’s share of electricity production – offer a cautionary tale of over-reliance on a single source of renewable energy. With hydropower stations mostly inherited from the Soviet times comes a dependence on aging infrastructure, continuous seasonal shortages, and crushing expansion costs.

In Kyrgyzstan, where the pace of glacial retreat due to rising annual temperatures continues to accelerate, the domestic hydropower generation has fallen 16 percent between 2018 and 2022. In the first half of 2025 the country had to import over 20 percent of all electricity consumed. To offset the persistent shortages, Kyrgyzstan has embarked on modernization of the Toktogul HPP, the country’s largest, planning to add an additional 240 MW to the current 1200 MW of installed capacity. The country also continues to expand its large hydropower cascade – including the upcoming construction of Kambarata HPP jointly funded by Kyrgyzstan, Kazakhstan and Uzbekistan. However, due to the highly capital-intensive nature of hydropower, ensuring sustainable financing is a complex task, requiring institutional investors and international assistance.

Beyond large hydropower plants, Kyrgyzstan aims to diversify its renewable electricity supply up to 10 percent of total generation by 2040. In addition to smaller HPPs, solar plant construction has gained pace in 2025 with a major 100 MW site planned in Chuy, near the country’s capital, Bishkek, and an ambitious $2 billion 1900 MW project in Issyk Kul region. However, another major energy project announced this year – 1200 MW Kara Keche thermal power plant – will rely on local coal, and so does the Bishkek Power Plant, which provides almost the entire electricity supply for the country’s capital. A planned transition to natural gas for the site may require almost as much gas as the entire country’s annual consumption.

Tajikistan, in turn, continues to struggle with its landmark Rogun HPP, set to be the largest in Central Asia with an installed capacity of almost 4000 MW upon completion. Once a source of political tension with its downstream neighbors dependent on Tajikistan for water supply, today Rogun poses a fundamental question of whether large hydropower projects in small developing economies are feasible at all.

The technical challenges of building the world’s tallest dam in harsh mountainous terrain are exacerbated by the mounting project costs. With only two out of eight planned turbines operational to date, Tajikistan needs to secure an additional $6.4 billion in funding, or almost double the amount of all state investments in the energy sector in over three decades, to complete the project by 2035. The World Bank is the project’s main investment coordinator. But with its $350 million loan under scrutiny, the Asian Infrastructure Investment Bank (AIIB) agreed to expand its funding from $270 million to $500 million. Other backers include the Saudi Fund for Development (SFD) and the Qatar Fund for Development (QFFD) with a $50 million loan, and yet Tajikistan continues to bear the bulk of the project costs, with over $450 million allocated from the budget since the beginning of 2025.

Tajikistan’s Green Energy Strategy-2037 outlines plans to expand energy generation capacity by additional 32.2 MW of hydropower, solar, and wind generation alongside with 2.51 MW of energy storage systems to provide power to remote areas. The government calls for investors to explore the country’s untapped green energy and hydropower potential along with various opportunities in natural resources exploration and offers tax and customs benefits and investors protection. However, for a relatively small landlocked economy, where remittances amount to the equivalent of almost half of GDP, green energy-driven economic diversification will remain contingent on economic factors beyond the government control.

In Kyrgyzstan, where the pace of glacial retreat due to rising annual temperatures continues to accelerate, the domestic hydropower generation has fallen 16 percent between 2018 and 2022. In the first half of 2025 the country had to import over 20 percent of all electricity consumed. To offset the persistent shortages, Kyrgyzstan has embarked on modernization of the Toktogul HPP, the country’s largest, planning to add an additional 240 MW to the current 1200 MW of installed capacity. The country also continues to expand its large hydropower cascade – including the upcoming construction of Kambarata HPP jointly funded by Kyrgyzstan, Kazakhstan and Uzbekistan. However, due to the highly capital-intensive nature of hydropower, ensuring sustainable financing is a complex task, requiring institutional investors and international assistance.

Beyond large hydropower plants, Kyrgyzstan aims to diversify its renewable electricity supply up to 10 percent of total generation by 2040. In addition to smaller HPPs, solar plant construction has gained pace in 2025 with a major 100 MW site planned in Chuy, near the country’s capital, Bishkek, and an ambitious $2 billion 1900 MW project in Issyk Kul region. However, another major energy project announced this year – 1200 MW Kara Keche thermal power plant – will rely on local coal, and so does the Bishkek Power Plant, which provides almost the entire electricity supply for the country’s capital. A planned transition to natural gas for the site may require almost as much gas as the entire country’s annual consumption.

Tajikistan, in turn, continues to struggle with its landmark Rogun HPP, set to be the largest in Central Asia with an installed capacity of almost 4000 MW upon completion. Once a source of political tension with its downstream neighbors dependent on Tajikistan for water supply, today Rogun poses a fundamental question of whether large hydropower projects in small developing economies are feasible at all.

The technical challenges of building the world’s tallest dam in harsh mountainous terrain are exacerbated by the mounting project costs. With only two out of eight planned turbines operational to date, Tajikistan needs to secure an additional $6.4 billion in funding, or almost double the amount of all state investments in the energy sector in over three decades, to complete the project by 2035. The World Bank is the project’s main investment coordinator. But with its $350 million loan under scrutiny, the Asian Infrastructure Investment Bank (AIIB) agreed to expand its funding from $270 million to $500 million. Other backers include the Saudi Fund for Development (SFD) and the Qatar Fund for Development (QFFD) with a $50 million loan, and yet Tajikistan continues to bear the bulk of the project costs, with over $450 million allocated from the budget since the beginning of 2025.

Tajikistan’s Green Energy Strategy-2037 outlines plans to expand energy generation capacity by additional 32.2 MW of hydropower, solar, and wind generation alongside with 2.51 MW of energy storage systems to provide power to remote areas. The government calls for investors to explore the country’s untapped green energy and hydropower potential along with various opportunities in natural resources exploration and offers tax and customs benefits and investors protection. However, for a relatively small landlocked economy, where remittances amount to the equivalent of almost half of GDP, green energy-driven economic diversification will remain contingent on economic factors beyond the government control.

Looking Ahead: Green Corridors and Energy Rings

The green energy trajectory of Central Asia is less about reckoning and more about rebalancing. For the larger industrialized economies of Kazakhstan and Uzbekistan, energy demands continues to outpace power generation. Renewable projects alone will not allow them to close this gap in the foreseeable future, but their overall scale and relative share in the energy mix will continue to grow. Kyrgyzstan and Tajikistan, in turn, will be expanding renewable generation – especially solar and wind – to somewhat offset the dependence on hydropower that provides cheaper energy but is costly and complex to expand.

Importantly, beyond questions of costs and efficiency, renewables offer the region substantial socio-economic and even political dividends. At the local level, renewable sites not only provide electricity to communities, they create employment opportunities in construction, servicing, and increasingly domestic components production. The competencies acquired by the local workforce in corporate training centers may also be deployed in Azerbaijan and other countries, where Gulf multinationals, such as ACWA Power, are expanding their green energy footprint.

Renewable energy is also among the key drivers of the regional integration – from the restoration of the Soviet-era Unified Energy System (Central Asia Energy Ring) to offset seasonal energy disbalances between the upstream and downstream countries to the trilateral Kyrgyz-Kazakh-Uzbek consortium to construct the Kambarata HPP. Moreover, renewable energy also ties Afghanistan closer to the region, with over half of the country’s electricity supplied by Tajikistan, and the rest by Uzbekistan and Turkmenistan, giving the Central Asian countries another economic and diplomatic leverage over their complicated and turbulent neighbor.

Green energy, along with the expansion of the Middle Corridor, redraws Central Asia’s trade flows. Beyond potential access to the lucrative European markets – most notably through the Green Corridor jointly developed by Kazakhstan, Uzbekistan, and Azerbaijan – Europe’s energy transition also drives the demand for Central Asia’s vast critical minerals resources. Tajik and Kyrgyz hydropower, in turn, revived CASA-1000, an ambitious project to connect Central and South Asia that would transport seasonal electricity surplus to Afghanistan and Pakistan. Renewables also drive billions of dollars in FDI inflows, making the region one of the major destinations for investors from the Gulf, China and Europe.

The future of energy transition as the driver of regional economic growth depends on several interlocking factors. Most critically, the region’s financial sustainability, which allows attracting long-term investments for renewables, as well as grid modernization, will be next to impossible without moving away from domestic energy subsidies. To balance lower domestic prices with profitable exports, countries would have to build enough capacity to generate electricity well in excess of domestic consumption. The distant export markets, in turn, would not only have to become reachable, meaning even more coordinated investments in energy transmission across vast territories and complex terrains, but remain accessible from geopolitical, regulatory and economic perspectives.

While favorable development on any of those factors is far from guaranteed, Central Asian governments have shown an ability to adapt to shifting global and domestic trends. Their approach to energy transition reflects this pragmatism: neither a wholesale embrace of renewables nor a retreat to hydrocarbons, but a nuanced recalibration of priorities in line with fiscal constraints, geopolitical realities, and technological opportunity.

Importantly, beyond questions of costs and efficiency, renewables offer the region substantial socio-economic and even political dividends. At the local level, renewable sites not only provide electricity to communities, they create employment opportunities in construction, servicing, and increasingly domestic components production. The competencies acquired by the local workforce in corporate training centers may also be deployed in Azerbaijan and other countries, where Gulf multinationals, such as ACWA Power, are expanding their green energy footprint.

Renewable energy is also among the key drivers of the regional integration – from the restoration of the Soviet-era Unified Energy System (Central Asia Energy Ring) to offset seasonal energy disbalances between the upstream and downstream countries to the trilateral Kyrgyz-Kazakh-Uzbek consortium to construct the Kambarata HPP. Moreover, renewable energy also ties Afghanistan closer to the region, with over half of the country’s electricity supplied by Tajikistan, and the rest by Uzbekistan and Turkmenistan, giving the Central Asian countries another economic and diplomatic leverage over their complicated and turbulent neighbor.

Green energy, along with the expansion of the Middle Corridor, redraws Central Asia’s trade flows. Beyond potential access to the lucrative European markets – most notably through the Green Corridor jointly developed by Kazakhstan, Uzbekistan, and Azerbaijan – Europe’s energy transition also drives the demand for Central Asia’s vast critical minerals resources. Tajik and Kyrgyz hydropower, in turn, revived CASA-1000, an ambitious project to connect Central and South Asia that would transport seasonal electricity surplus to Afghanistan and Pakistan. Renewables also drive billions of dollars in FDI inflows, making the region one of the major destinations for investors from the Gulf, China and Europe.

The future of energy transition as the driver of regional economic growth depends on several interlocking factors. Most critically, the region’s financial sustainability, which allows attracting long-term investments for renewables, as well as grid modernization, will be next to impossible without moving away from domestic energy subsidies. To balance lower domestic prices with profitable exports, countries would have to build enough capacity to generate electricity well in excess of domestic consumption. The distant export markets, in turn, would not only have to become reachable, meaning even more coordinated investments in energy transmission across vast territories and complex terrains, but remain accessible from geopolitical, regulatory and economic perspectives.

While favorable development on any of those factors is far from guaranteed, Central Asian governments have shown an ability to adapt to shifting global and domestic trends. Their approach to energy transition reflects this pragmatism: neither a wholesale embrace of renewables nor a retreat to hydrocarbons, but a nuanced recalibration of priorities in line with fiscal constraints, geopolitical realities, and technological opportunity.

This article was originally published by The Diplomat