SOEs in Central Asia

The state-owned enterprises (SOEs) in Central Asia play a critical role in economic development. The local SOEs and quasi-state entities control critical sectors of the economy and account for a large share of GDP and employment. In many ways, this situation is not unique to developing economies, as EBRD cross-country analysis of 20 developing countries indicates that SOEs dominate the utility and transport sectors, but are also present in agriculture, energy, construction, and even trade.

In Central Asia, this issue is further exacerbated by the state’s overwhelming presence in almost every sector even following several privatization waves. According to the ADB study, the two largest economies in the region - Kazakhstan and Uzbekistan - had over 6000 and 2000 operational SOEs respectively, controlling key assets in the most critical sectors, and often holding a monopoly or quasi-monopoly position in those. In some cases, the SOEs even have regulatory functions, further enhancing their weight in influence in the market at the cost of the private sector.

While the overall inefficiencies of SOEs compared to the private sector are well known, the economic performance of SOEs is uneven and varies from country to country and sector to sector. For instance, in Kyrgyzstan state-owned entities in most sectors except one are profitable, while in Uzbekistan almost 10% of SOEs reported significant losses. However, SOE’s economic results analysis have also to account for various tax and customs preferences, preferential access to public funds for their investment programs, and subsidized loans from the state-owned banks along with other off-budget subsidies and incentives not available to private entities.

On the other hand, SOEs are often tasked with developing industrial capacity and infrastructure development, providing employment and social guarantees to hundreds of thousands of people (up to 37% of the workforce in Uzbekistan, for example), with the national development policies justifying their preferential treatment. More so, in the last few years, Kazakhstan and Kyrgyzstan reversed the earlier privatization of some key industrial assets, as the MNCs controlling the local operations either failed to meet the security standards or were unable to fulfill the expectations of social and economic benefits.

The dominance of SOEs in the nations’ economies thus plays a critical and complex role in economic growth, and governments are understandably reluctant to fully relinquish their control over strategic assets for a variety of reasons, including economic and social security.

Nonetheless, without major governance reforms, SOEs will continue to underperform economically while siphoning away public funds to sustain their operations. The varying approaches of the Central Asian countries to reforms aimed at increasing the efficiency and competitiveness of the local SOEs illustrate the complexity of such a task and the limits of balancing between governmental control and economic performance.

The state-owned enterprises (SOEs) in Central Asia play a critical role in economic development. The local SOEs and quasi-state entities control critical sectors of the economy and account for a large share of GDP and employment. In many ways, this situation is not unique to developing economies, as EBRD cross-country analysis of 20 developing countries indicates that SOEs dominate the utility and transport sectors, but are also present in agriculture, energy, construction, and even trade.

In Central Asia, this issue is further exacerbated by the state’s overwhelming presence in almost every sector even following several privatization waves. According to the ADB study, the two largest economies in the region - Kazakhstan and Uzbekistan - had over 6000 and 2000 operational SOEs respectively, controlling key assets in the most critical sectors, and often holding a monopoly or quasi-monopoly position in those. In some cases, the SOEs even have regulatory functions, further enhancing their weight in influence in the market at the cost of the private sector.

While the overall inefficiencies of SOEs compared to the private sector are well known, the economic performance of SOEs is uneven and varies from country to country and sector to sector. For instance, in Kyrgyzstan state-owned entities in most sectors except one are profitable, while in Uzbekistan almost 10% of SOEs reported significant losses. However, SOE’s economic results analysis have also to account for various tax and customs preferences, preferential access to public funds for their investment programs, and subsidized loans from the state-owned banks along with other off-budget subsidies and incentives not available to private entities.

On the other hand, SOEs are often tasked with developing industrial capacity and infrastructure development, providing employment and social guarantees to hundreds of thousands of people (up to 37% of the workforce in Uzbekistan, for example), with the national development policies justifying their preferential treatment. More so, in the last few years, Kazakhstan and Kyrgyzstan reversed the earlier privatization of some key industrial assets, as the MNCs controlling the local operations either failed to meet the security standards or were unable to fulfill the expectations of social and economic benefits.

The dominance of SOEs in the nations’ economies thus plays a critical and complex role in economic growth, and governments are understandably reluctant to fully relinquish their control over strategic assets for a variety of reasons, including economic and social security.

Nonetheless, without major governance reforms, SOEs will continue to underperform economically while siphoning away public funds to sustain their operations. The varying approaches of the Central Asian countries to reforms aimed at increasing the efficiency and competitiveness of the local SOEs illustrate the complexity of such a task and the limits of balancing between governmental control and economic performance.

Centralization Model: Kazakhstan

Kazakhstan, the largest economy in the region, was among the first to introduce the model of holding companies for SOE management. Created in 2008, the national wealth fund Samruk-Kazyna was reportedly modeled after Singapore’s conglomerate Temasek to improve corporate governance and increase the capitalization of the nation’s strategic companies. Samruk-Kazyna’s sole stakeholder is the Government of the Republic of Kazakhstan, and the fund is a major or sole shareholder of many of Kazakhstan’s largest companies, including KazMunayGaz, Kazakhtelecom, KazTransOil, Air Astana, and the national grid operator KEGOC, overall accounting for about 30% of the nation’s GDP.

Kazakhstan, the largest economy in the region, was among the first to introduce the model of holding companies for SOE management. Created in 2008, the national wealth fund Samruk-Kazyna was reportedly modeled after Singapore’s conglomerate Temasek to improve corporate governance and increase the capitalization of the nation’s strategic companies. Samruk-Kazyna’s sole stakeholder is the Government of the Republic of Kazakhstan, and the fund is a major or sole shareholder of many of Kazakhstan’s largest companies, including KazMunayGaz, Kazakhtelecom, KazTransOil, Air Astana, and the national grid operator KEGOC, overall accounting for about 30% of the nation’s GDP.

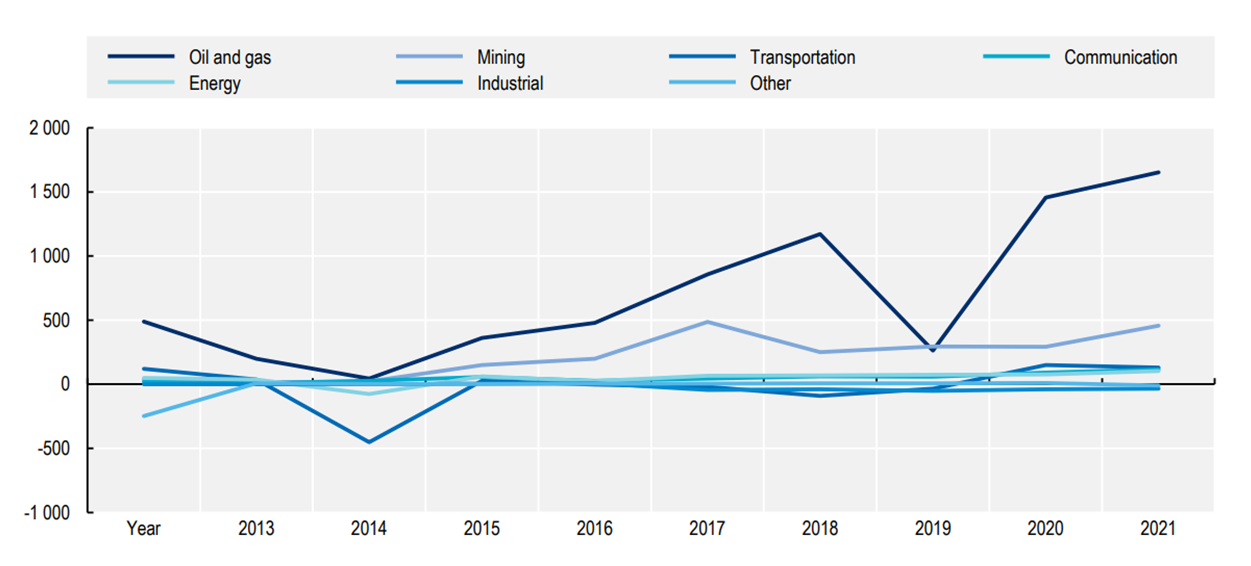

Samruk-Kazyna Net Profit (in thousand KZT), Source: OECD

Samruk-Kazyna operates under its own Sovereign Wealth Fund (SWF) Law, which according to the World Bank is in line with good international practice. While the government exercises its sole shareholder rights through the Board of Directors (BOD), chaired by the Prime Minister, it nonetheless has the policy of non-interference with Samruk-Kazyna operational activities, and state bodies representatives are prohibited from the BOD roles at the fund’s portfolio companies. With the fund’s management and reporting practices built upon the market economy principles, in the last three years, the holding reported continuing growth in most of its sectors.

However, the question of whether the fund enabled more market-like and competitive functioning of its portfolio companies and reduced the state's role in the economy remains open. Samruk-Kazyna, according to some analysts, continues to cross-subsidize its portfolio companies to compensate for other government subsidies and reduced tariffs - from gas prices to railroad tickets - while at the same time running ambitious investment programs. The fund also runs a high debt to the government and external lenders, resulting in the government capping the fund’s external debt at $12.5 bln in 2024 to balance the state budget.

The results of state assets privatization, in which Samruk-Kazyna plays a critical role as the owner of companies planned for initial public offerings (the so-called “People IPO”), were mixed as well. The public offering of some key portfolio companies through the ‘People IPO’ was delayed and the very concept of privatizing state assets through floating shares on the local stock exchanges was itself put into question. Nonetheless, in 2023-24 the fund sold some of its assets in mining, energy, and telecom to private investors, and Air Astana, the national air carrier and Samruk-Kazyna portfolio company, went public on LSE this spring.

Notwithstanding criticism of Samruk-Kazyna management and lack of transparency compared to SWFs in developed economies, including from the Kazakh President himself, it remains the most advanced mechanism of SOE management in the region, prominently featured in the Comprehensive Privatization Plan. The SWF clearly served as a model for the neighboring Kyrgyzstan reform of its own SOE sector, including the recently announced establishment of the National Investment Fund of the Kyrgyz Republic.

Notably, of all Central Asian countries, Kyrgyzstan ran the most comprehensive privatization in the early 90s and currently owns fewer SOEs than its neighbors (around 136). However, in various forms, the state has retained control over the most critical sectors, including mining, transportation, and energy. The latter sector, in particular, presents the most pressing challenge with continuing losses covered by the state coffers. Additionally, ambitious projects in regional transportation connectivity and renewable energy require better financial and management discipline and will likely be the focus of the continuing SOE reform.

However, the question of whether the fund enabled more market-like and competitive functioning of its portfolio companies and reduced the state's role in the economy remains open. Samruk-Kazyna, according to some analysts, continues to cross-subsidize its portfolio companies to compensate for other government subsidies and reduced tariffs - from gas prices to railroad tickets - while at the same time running ambitious investment programs. The fund also runs a high debt to the government and external lenders, resulting in the government capping the fund’s external debt at $12.5 bln in 2024 to balance the state budget.

The results of state assets privatization, in which Samruk-Kazyna plays a critical role as the owner of companies planned for initial public offerings (the so-called “People IPO”), were mixed as well. The public offering of some key portfolio companies through the ‘People IPO’ was delayed and the very concept of privatizing state assets through floating shares on the local stock exchanges was itself put into question. Nonetheless, in 2023-24 the fund sold some of its assets in mining, energy, and telecom to private investors, and Air Astana, the national air carrier and Samruk-Kazyna portfolio company, went public on LSE this spring.

Notwithstanding criticism of Samruk-Kazyna management and lack of transparency compared to SWFs in developed economies, including from the Kazakh President himself, it remains the most advanced mechanism of SOE management in the region, prominently featured in the Comprehensive Privatization Plan. The SWF clearly served as a model for the neighboring Kyrgyzstan reform of its own SOE sector, including the recently announced establishment of the National Investment Fund of the Kyrgyz Republic.

Notably, of all Central Asian countries, Kyrgyzstan ran the most comprehensive privatization in the early 90s and currently owns fewer SOEs than its neighbors (around 136). However, in various forms, the state has retained control over the most critical sectors, including mining, transportation, and energy. The latter sector, in particular, presents the most pressing challenge with continuing losses covered by the state coffers. Additionally, ambitious projects in regional transportation connectivity and renewable energy require better financial and management discipline and will likely be the focus of the continuing SOE reform.

Sectoral Management Model: Uzbekistan

Uzbekistan, where the role of the state in general and SOE in particular in the economy is far more prominent, took a markedly different path with regard to the management of state-owned enterprises. While some smaller companies in the service and commerce sectors were privatized through various means in the early 90s, to this day the SOEs not only dominate the ‘commanding heights’ in the key sectors but are present across all industries and companies of all sizes. The official statistics on the share of SOEs in GDP are scant, but ADB experts estimate that at the start of economic reforms in 2017, such enterprises accounted for 47% of industrial output and about 37% of employment.

With SOEs traditionally seen as the key drivers of the nation’s industrial development, Uzbekistan largely retained the ‘sector-specific’ structure, where large SOEs oversee the management of enterprises as well as implementation of industrial development policies within the assigned segment, as opposed to a single centralized holding to manage them all. Although the majority of SOEs are incorporated as Joint Stock Companies, the government is often either a sole or a majority stakeholder of those, with the shares spread across several government agencies, and the enterprises themselves are controlled by supervisory boards chaired by the relevant ministers (up to the prime minister level).

Incentivizing the operational efficiency of SOEs is further complicated by the structure of Uzbekistan’s economy. While 90% of SOEs are monopolies in their respective industries, they operate in the market with heavily regulated prices where price gaps are covered by various budget subsidies. Receiving those subsidies, along with many other instruments of direct and indirect financial support from the state budget, would be impossible to private sector players, and raising tariffs to economically viable levels would mean risking galloping inflation and potential social unrest.

Thus, the government’s approach to SOEs following the start of structural reforms post-2017 seems to be two-pronged. On the one hand, the government continues to offload some state property and shares to the private sector and international investors through the State Assets Management Agency’s auctions. On the other, it introduces a more level-playing field by curbing the dominant position of the ‘natural monopolies’ (read SOEs) and inviting more competition from private enterprises. At the same time, the state retains complete ownership or a majority stake in the largest enterprises across numerous sectors - from banking and telecom to mining and energy.

Uzbekistan, where the role of the state in general and SOE in particular in the economy is far more prominent, took a markedly different path with regard to the management of state-owned enterprises. While some smaller companies in the service and commerce sectors were privatized through various means in the early 90s, to this day the SOEs not only dominate the ‘commanding heights’ in the key sectors but are present across all industries and companies of all sizes. The official statistics on the share of SOEs in GDP are scant, but ADB experts estimate that at the start of economic reforms in 2017, such enterprises accounted for 47% of industrial output and about 37% of employment.

With SOEs traditionally seen as the key drivers of the nation’s industrial development, Uzbekistan largely retained the ‘sector-specific’ structure, where large SOEs oversee the management of enterprises as well as implementation of industrial development policies within the assigned segment, as opposed to a single centralized holding to manage them all. Although the majority of SOEs are incorporated as Joint Stock Companies, the government is often either a sole or a majority stakeholder of those, with the shares spread across several government agencies, and the enterprises themselves are controlled by supervisory boards chaired by the relevant ministers (up to the prime minister level).

Incentivizing the operational efficiency of SOEs is further complicated by the structure of Uzbekistan’s economy. While 90% of SOEs are monopolies in their respective industries, they operate in the market with heavily regulated prices where price gaps are covered by various budget subsidies. Receiving those subsidies, along with many other instruments of direct and indirect financial support from the state budget, would be impossible to private sector players, and raising tariffs to economically viable levels would mean risking galloping inflation and potential social unrest.

Thus, the government’s approach to SOEs following the start of structural reforms post-2017 seems to be two-pronged. On the one hand, the government continues to offload some state property and shares to the private sector and international investors through the State Assets Management Agency’s auctions. On the other, it introduces a more level-playing field by curbing the dominant position of the ‘natural monopolies’ (read SOEs) and inviting more competition from private enterprises. At the same time, the state retains complete ownership or a majority stake in the largest enterprises across numerous sectors - from banking and telecom to mining and energy.

Top 10 Uzbekistan's SOEs taxes in Q1 2024, source: Daryo

Despite the clear financial benefits of further privatization, the expectations that larger SOEs could soon be privatized through the People IPOs have so far proven to be premature. Unlike Kazakhstan, which attracts foreign capital and retail investors to take part in privatization through a dual-track listing of SOE shares on the Kazakhstan Stock Exchange (KASE) and Astana International Exchange (AIX), registered in a special jurisdiction under the English common law principles, Uzbekistan’s stock market remains at the nascent stage. The limited listings of two SOEs' shares on the Tashkent Stock Exchange last year had neither significantly raised the companies' value nor greatly increased investors’ activity.

This setback has likely led to the revision of SOE privatization plans, making external platforms more attractive than local ones. For instance, the deadlines for the long-awaited privatization of the banking sector were extended further, and the 40% target of state ownership share in the sector by 2025 will likely be missed. Similarly, the listing of the shares of the nation’s largest taxpayer and the world’s top four gold producer Navoi Metallurgical and Mining Combinat (NMMC), will likely take place no earlier than next year and be limited to 2% to 5%.

This setback has likely led to the revision of SOE privatization plans, making external platforms more attractive than local ones. For instance, the deadlines for the long-awaited privatization of the banking sector were extended further, and the 40% target of state ownership share in the sector by 2025 will likely be missed. Similarly, the listing of the shares of the nation’s largest taxpayer and the world’s top four gold producer Navoi Metallurgical and Mining Combinat (NMMC), will likely take place no earlier than next year and be limited to 2% to 5%.

The Road Ahead

Increasingly, the quasi-state dominance in the market economy of Central Asia is seen as a significant roadblock to attracting much-needed investments as well as to continuous economic growth. Nonetheless, the dominance of SOEs will remain a notable feature of the regional economic landscape for the foreseeable future.

Despite the different structures of SOE management in Kazakhstan and Uzbekistan, their economic performance often lacks the private sector’s dynamism. The reforms of SOE governance along the lines of commercial enterprises, while clearly needed, may not be sufficient. The primary challenge lies in balancing the national industrial and infrastructure development policies, of which SOEs remain the primary instrument, and states’ budgets, of which SOEs are simultaneously the main donors and the main beneficiaries.

While further privatization of the Central Asian SOEs is almost inevitable to achieve the countries’ growth targets, this process will be gradual, often inconsistent, likely prolonged, and clearly subject to other structural reforms ranging from capital markets to consumer prices and tariffs.

Increasingly, the quasi-state dominance in the market economy of Central Asia is seen as a significant roadblock to attracting much-needed investments as well as to continuous economic growth. Nonetheless, the dominance of SOEs will remain a notable feature of the regional economic landscape for the foreseeable future.

Despite the different structures of SOE management in Kazakhstan and Uzbekistan, their economic performance often lacks the private sector’s dynamism. The reforms of SOE governance along the lines of commercial enterprises, while clearly needed, may not be sufficient. The primary challenge lies in balancing the national industrial and infrastructure development policies, of which SOEs remain the primary instrument, and states’ budgets, of which SOEs are simultaneously the main donors and the main beneficiaries.

While further privatization of the Central Asian SOEs is almost inevitable to achieve the countries’ growth targets, this process will be gradual, often inconsistent, likely prolonged, and clearly subject to other structural reforms ranging from capital markets to consumer prices and tariffs.